Back in September, HMRC issued its latest pensions stats and figures, covering the 2020/21 tax year.

The report gives a fascinating glimpse into the choices pensioners, and those saving toward their retirement, are making, and the cost of those decisions.

From the numbers of UK workers opting for flexible pension options to tax relief claims and the value of Lifetime Allowance (LTA) receipts, keep reading for everything you need to know.

Contributions are on the rise, but not into workplace pensions

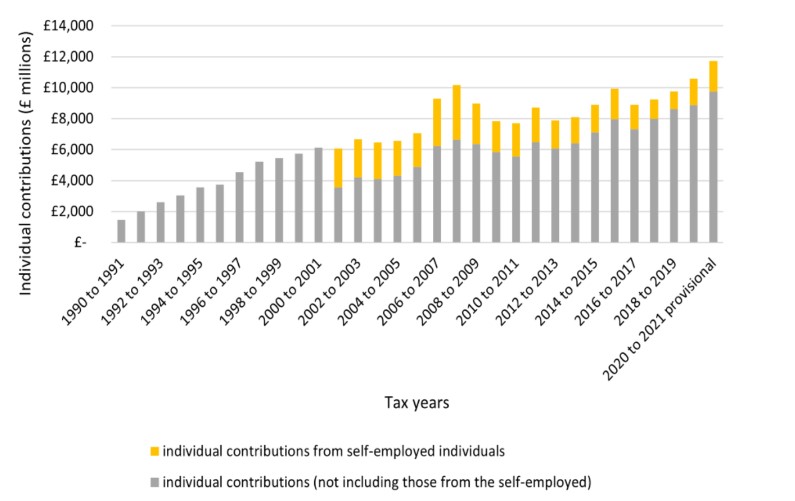

The latest figures for 2020/21 confirm that individuals contributed £11.7 billion to their personal pensions. This marked an increase of more than 10% from 2019/20.

Interestingly, the increase among the self-employed topped 17%, despite continued concern that this group are in the most danger of having a pension shortfall at retirement.

The value of individual contributions to personal pension schemes from 1990/91 to 2020/21:

Source: HMRC

Numbers paying into workplace pensions took a huge dip in 2020/21, from 5.6 million to just short of 3.2 million.

The dip is likely due, at least partly, to the effect of Covid on the whole of the UK workforce during 2020/21. Furloughing, redundancies, and money worries for many meant that pensions were sacrificed.

Pensions Research 2020, a report from Employee Benefits, found that during Covid:

- 16% of employees reduced their pension contribution levels

- 7% stopped their contributions but remained opted in

- 15% opted out of their workplace pension scheme altogether.

While Covid is no doubt partly responsible, a recent FTAdviser report suggests another worrying factor. The article confirms the results of a recent survey which found that more than a third (34%) of respondents had never heard of auto-enrolment.

The frozen LTA makes careful planning more important than ever

Last year, then-chancellor Rishi Sunak used his Spring Budget to freeze the LTA.

Introduced back in 2006, the LTA limits the amount you can withdraw from your pensions before triggering an LTA charge. The charge is 55% on excess funds taken as a lump sum and 25% where funds are taken as income.

As pension values rise, the frozen allowance (of £1,073,100) was expected to see more people hit with a charge.

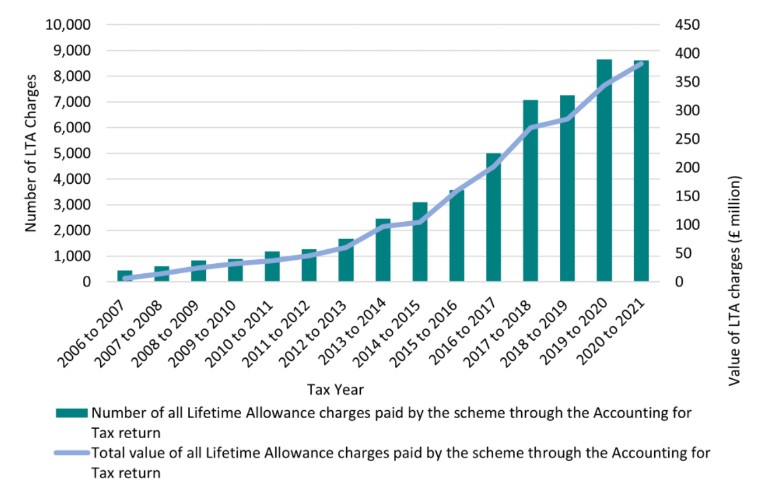

Recent HMRC figures suggest that this has been the case. While the total number of charges fell (albeit only by 0.5%), the total value of those charges increased by 11%. Treasury receipts totalled £382 million.

Reported number and value of LTA charges through Accounting For Tax (AFT) from 2006/07 to 2020/21:

Source: HMRC

When the freeze was announced (as part of Sunak’s plan to balance the books post-Covid) it was expected to raise around £990 million. Recent reports suggest that Jeremy Hunt may look to extend the freeze.

This move would increase Treasury income from the charge and from “saved” tax relief as people cease contributions to avoid hitting the limit. It also highlights the need to think carefully about the amount you’re contributing.

Remember, expert financial advice can help you to manage your pension tax-efficiently so get in touch if you have any questions.

The cost of living crisis might be partly to blame for an upturn in flexible withdrawals

HMRC reports that since Pension Freedoms legislation was introduced in 2015, taxable payment values have exceeded £59 billion.

During 2021/22, £10.6 billion in taxable payments was withdrawn from pensions flexibly. This figure includes £3.6 billion withdrawn by 508,000 individuals during Q2 of 2022 alone. The figure marks a 23% increase compared to the same period in 2021.

The reported value of taxable flexibly accessed payments and the number of individuals accessing these payments each quarter (Q3 2017 to Q2 2022):

Source: HMRC

The huge increase in flexible pension withdrawals could be due to the current cost of living crisis. While it would be hoped that a resilient long-term financial plan would render unscheduled withdrawals unnecessary, this might not be the case for those without an adviser.

At HDA, we can help you to stay on top of your household budgeting whatever happens in the wider world of finance. This means you can continue to pay your future self and keep your long-term plans on track.

Get in touch

If you’d like to discuss your pension or any other aspect of your long-term financial plans, we can help. Please get in touch via email at enquiries@hda-ifa.co.uk or call 01242 514563.

Please note

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

Workplace pensions are regulated by The Pension Regulator.