The last few years have seen volatile markets react to a global pandemic, soaring inflation amid a cost of living crisis, and a war in Ukraine.

Markets are expected to rise and fall, but remaining unemotional about your investments isn’t always easy.

Thankfully, several valuable lessons can help you to stay calm and stress-free, whatever global events and markets throw at you.

Here are five important lessons to learn now.

1. Markets fluctuate daily but your focus should be on the long term

Stock market prices rise and fall daily, reacting to investor confidence and myriad other factors.

When events like the pandemic or Russia’s invasion of Ukraine create global uncertainty, the result is likely to be short-term economic uncertainty.

This graph shows the FTSE All-Share Index since June 2022 and the ups and downs of the market are clear.

Source: London Stock Exchange

The graph shows only the last 12 months, beginning long after the height of the coronavirus pandemic and four months after the beginning of the war in Ukraine.

While the tumultuousness of these 12 months is clear, it’s important to remember that this is a short-term outlook whereas your investments are intended as long-term propositions.

We recommend investing only with a clear goal in mind, which is ideally 5 to 10 years away. This gives plenty of time for your wealth to ride out any short-term bumps in the road so staying focused on this long-term goal is key.

That means not checking in with your investment daily, which could lead to stress. Instead, check in only regularly enough to make sure that your plans remain on track.

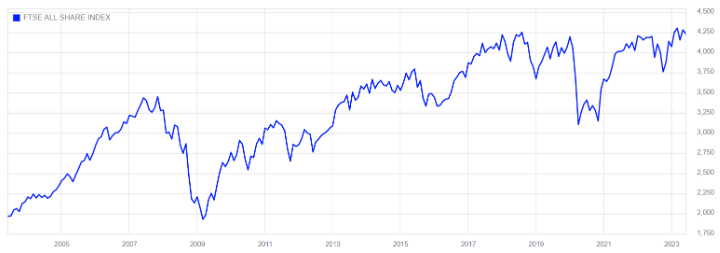

2. Generally, the trend of the markets is upward

Contrast the FTSE All-Share Index for the last 12 months with its performance since June 2003 and you will see that the general trend has been upwards.

Source: London Stock Exchange

This 20-year period shows the effect of the 2008 global financial crisis and the onset of the pandemic in 2020.

And yet the general rise is clear. Short periods of volatility cause sharp drops in value but are generally followed by sustained periods of recovery, which tend to last longer and be sufficient to offset the fall.

Checking your investment daily and becoming stressed during market dips could result in you selling off your shares. This not only makes a paper loss into a real one, but it also means your funds won’t be invested when the market recovers, and you’ll miss out on the returns as markets rise.

3. The stock market isn’t the economy

The cost of living crisis has dominated headlines for some time, with inflation peaking at a 40-year high and energy bills soaring.

With UK economic policy and forecasts all over the news, worrying about your own wealth is understandable. In these circumstances, though, it pays to remember that the stock market is not the economy.

The markets are based on investor confidence, so economic uncertainty is often reflected in the markets long before a recession arrives. Upturns are often visible in the markets in advance of a recession’s official end.

It’s also important to remember that the indexes we look at – the FTSE 100, the FTSE All-Share, and the S&P500 – are made up of huge companies with global profits.

UK unemployment rises or local businesses struggling to make ends meet are unlikely to make much of a dent in these indexes, which can continue to generate returns from companies’ huge revenue and global reach.

4. Diversification spreads your investment risk

Watching an index like the FTSE All-Share drop suddenly, as it did in February and March 2020, can be stressful. But it’s important to remember that your investments aren’t held in one place.

Your funds are diversified, which means they are invested across asset classes, sectors, and geographical regions. This is done specifically to spread risk so that a drop in one area will hopefully be offset by a rise elsewhere.

It is for this reason that a 5% drop in a specific index won’t automatically mean a 5% drop in the value of your holdings.

5. With inflation high, your cash savings could be losing “real terms” value

Finally, inflation might have peaked back in October 2022 – at a 40-year high of 11.1% – but it remains high. It is falling, but only slowly, and could still take two years to return to the Bank of England’s 2% target.

The Consumer Prices Index (CPI) since March 2013:

Source: Office for National Statistics (ONS)

The interest you receive on your cash holdings is likely to be lower than inflation, diminishing your savings’ buying power. Your money is effectively losing value in real terms.

Investing might offer the means to tackle inflation, by seeing higher returns for additional risk. And while that risk might seem stressful, the biggest risk to your wealth could be not taking enough risk.

Get in touch

If you’re worried about the effects of short-term volatility on your investments, or any other aspect of your long-term financial plans, we can help. Please get in touch via email at enquiries@hda-ifa.co.uk or call 01242 514563.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.